The current regional ceasefire provides a vital window for supply chain stabilisation. However, the transition from disruption to normalisation is not instantaneous. For freight forwarders and cargo owners, the primary challenge has shifted from active risk avoidance to managing significant volume backlogs across all modes of transport.

Ocean Freight Recovery Timelines

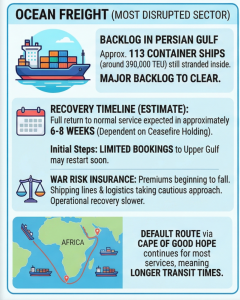

The maritime sector remains the most impacted by the recent instability. Approximately 113 container ships, representing 390,000 TEU, are currently positioned within the Persian Gulf.

-

Service Restoration: Full normalisation of schedules is estimated to take 6 to 8 weeks.

-

Current Routing: The Cape of Good Hope remains the default transit route for most carriers to avoid residual risks.

-

Upper Gulf Bookings: While limited bookings are expected to resume shortly, this remains contingent on the stability of the Strait of Hormuz.

Air Freight and Infrastructure Capacity

Air cargo is demonstrating a more agile recovery compared to sea freight. UAE airports are currently operating at 70 to 80 percent capacity, though several hurdles remain.

-

Operational Window: A return to pre-disruption capacity is expected within 3 to 6 weeks.

-

Constraints: Continued flight suspensions by international carriers and regional airspace restrictions are still influencing flight paths.

Regional Port and Hub Status Report

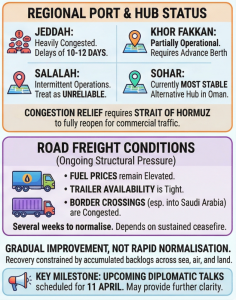

Strategic hubs across the GCC are experiencing varying levels of operational efficiency.

| Port / Hub | Current Status | Impact |

| Sohar | Stable | Currently the most reliable alternative hub in Oman. |

| Jeddah | Heavily Congested | Ongoing delays of 10 to 12 days. |

| Khor Fakkan | Partially Operational | Advance berth confirmation is mandatory. |

| Salalah | Intermittent | Service remains unreliable at this stage. |

Road Freight and Inland Logistics

Inland transport continues to face structural headwinds that will likely persist through the second quarter.

-

Operating Costs: Elevated fuel prices are expected to remain high in the short term.

-

Equipment Availability: Trailer supply remains tight across the GCC.

-

Border Crossings: Significant congestion continues, particularly at Saudi Arabian entry points.

The Strategic Outlook

The decline in war risk insurance premiums is a positive lead indicator, but it is not yet matched by operational fluidity. The upcoming diplomatic talks on 11 April serve as the next major milestone for the industry.

Actionable Advice for Shippers:

-

Prioritise Backlog Clearing: Factor in an additional 14 days for any cargo currently caught in the Persian Gulf backlog.

-

Utilise Stable Hubs: Divert urgent Middle East distributions through Sohar where possible.

-

Verify Tracking: Direct carrier updates are currently more reliable than automated tracking systems.